Risk Management

LCH represents the gold standard for CCP risk management

As part of the central counterparty services offering, LCH is responsible for risk management. This involves day-to-day risk management of cleared products, margining of Clearing Member positions, margin models, setting and analysing margin parameters, daily Member-level monitoring, and potentially intra-day margin calls.

In order to be confident that it can maintain the safety and stability of Clearing Members and clients, the Listed Rates Service has built a framework of safeguards, underpinned by state-of-the-art risk models.

These various layers of protection work in concert to ensure that LCH has adequate financial resources to fulfil these obligations in all circumstances - most importantly, to protect cleared trades at our clearing house and the collateral posted against them.

Membership Criteria

The Rates Service Membership Criteria are set out by LCH to promote financial soundness and form the first line of defence against a default.

Initial Margin

When new Members begin clearing Listed Rates trades, LCH collects initial margin from them to cover potential losses in the event of a default. We calculate initial margin using LCH’s Historical Expected Shortfall methodology, which uses five years of historical market data to estimate the potential loss distribution. We also apply margin add-ons covering credit risk and liquidity risk where a particular Member’s inherent risk exposure is not captured within the PAIRS model.

Variation Margin

In addition to initial margin, we also collect daily and intraday variation margin from all counterparties to account for changes in the mark-to-market value Listed Rates positions. Positions will be settled to market at the closing price provided by the Exchanges each day and margin payments will be processed by LCH.

By collecting variation margin, we ensure that all our Members are current on all obligations which prevent default scenarios where Member losses could have accumulated over a prolonged period of time.

Default Management

In the event of a Clearing Member default, these pre-emptive safeguards dramatically limit the impact arising from the default. The defaulted portfolio of listed contracts is either traded out or hedged to reduce its risk, which in turn makes the Rates Service task of auctioning and porting trades facing the defaulted member to healthy counterparties vastly easier.

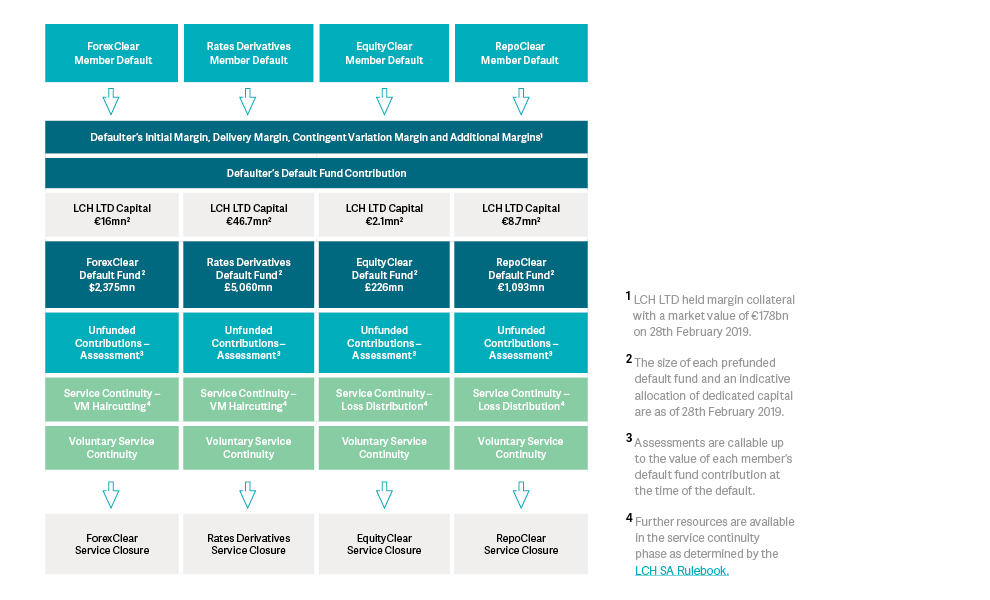

Default Fund

Following the Clearing Member default, our default waterfall model dictates that the defaulting Clearing Member’s posted margin and default fund contributions are the first resources to be consumed. Only after these resources are exhausted across all services and LCH’s own ‘skin-in-the-game’ is consumed would non-defaulting Clearing Members be exposed to losses.

LCH maintains a rigorous default management process.

LCH has a proven track record of handling defaults, managing the Lehman default ($9 trillion portfolio of 66,390 trades) and using only 35% of Lehman’s initial margin across all assets held at LCH.

Our default management process follows three steps to reduce the risk of the defaulting Clearing Member’s outstanding positions without impacting non-defaulting Clearing Members:

Risk Neutralisation & Client Porting: After a Clearing Member default, the defaulter's trade portfolio is traded out or hedged with the assistance of our Rates Service Default Management Group, made up of internal and external participants that are seconded to LCH in the event of default.

Alongside this, the Rates Service begins the process of attempting to port clients to non-defaulting Clearing Members. There is an established process in place for clients operating under each of the clearing models offered by the Rates Service.

Portfolio Auction: Where the listed portfolio has been hedged rather than traded out, the residual portfolios are auctioned to the membership. The ability to receive and price an auctioned portfolio is one of the criteria we verify prior to granting membership to LCH.

Loss Attribution: In the event that losses are greater than the financial resources of the defaulting member and of LCH, the funded Default Fund contributions of non-defaulting remaining rates members are used.

Losses arising from variation margin and hedges are attributed pro-rata, while losses arising from auctions are attributed based upon bidding behaviour in the auction.

LCH’s default waterfall establishes the order in which the financial resources of a defaulted Clearing Member, non-defaulting Clearing Members and the resources of LCH are consumed during the resolution of a default.

A defaulting Clearing Member’s posted initial margin is the first asset to be consumed in managing the default, followed by the defaulter’s contribution to the Rates Service Default Fund.

If these assets prove insufficient to resolve the default, LCH’s own capital is next in line for losses. It is only after all of these resources are exhausted that default fund contributions from non-defaulting Clearing Members are utilized.

In the extreme event that all default waterfall resources are consumed and defaulted positions have not been fully auctioned, an additional safety net will be triggered allowing the service to continue. This is the Loss Allocation stage, which sees Variation Margin Gains Haircutting (VMGH) applied to trades that have made profits since the point of default.